Social Security: Are You Leaving Money on the Table?

For many people nearing retirement, Social Security seems simple. You worked, you earned the benefit, and you start taking it when the time feels right.

But Social Security planning is rarely that straightforward.

At Independent Wealth Solutions, we regularly speak with individuals and couples who do not realize how much timing matters. In some cases, people may leave thousands of dollars on the table over the course of retirement by claiming too early, overlooking spousal strategies, or failing to coordinate Social Security with the rest of their financial plan.

For retirees and pre-retirees in North County San Diego, where the cost of living can be higher than many other parts of the country, making the most of every income source matters.

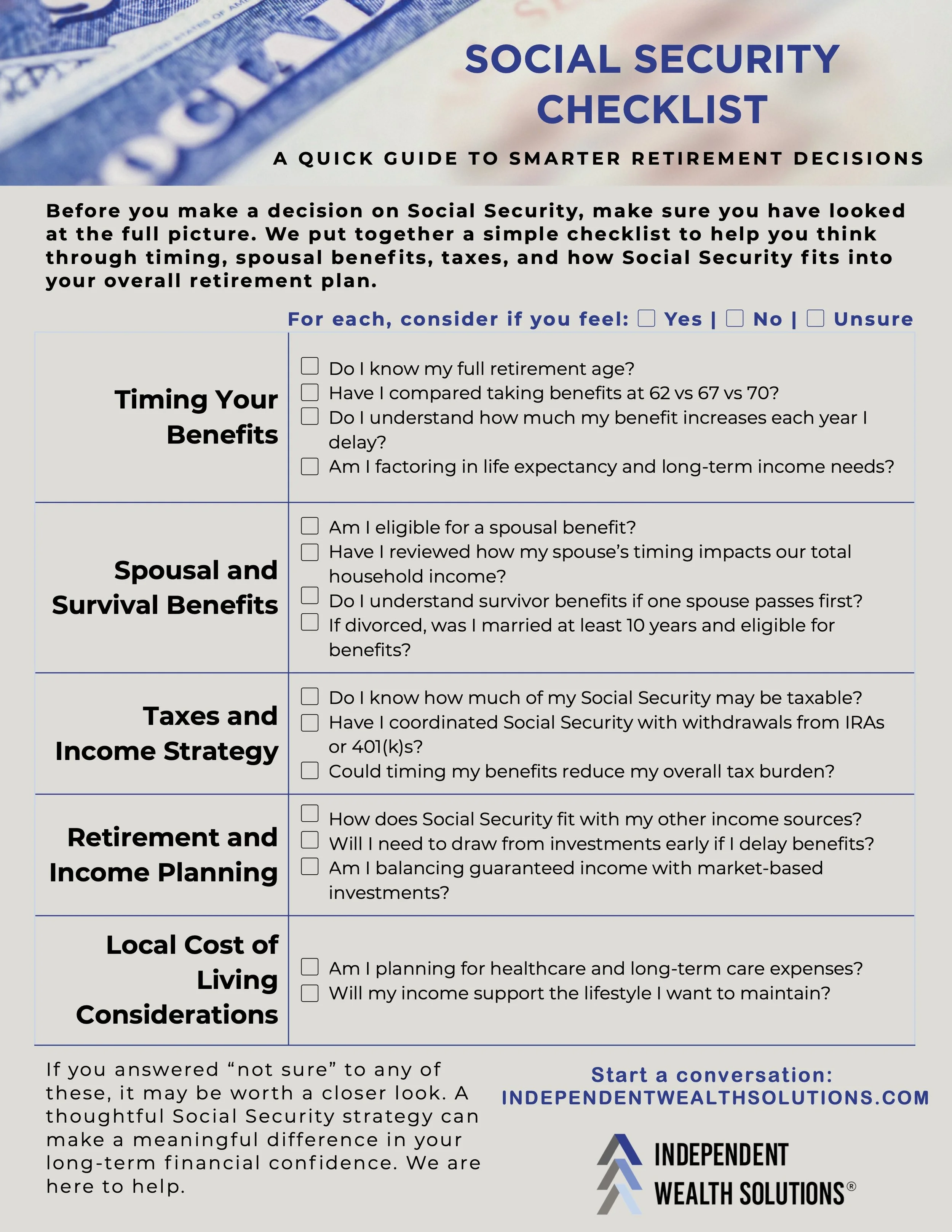

Not sure what’s important to consider regarding social security?

Download our checklist to learn more.

Why Social Security Timing Matters

One of the biggest retirement questions is simple: When should you take Social Security?

You can begin claiming as early as age 62, but taking benefits early reduces your monthly payment. Waiting until your full retirement age gives you your standard benefit, and delaying up to age 70 can increase your monthly benefit even more.

Here is the basic tradeoff:

Claim at 62 and receive a reduced monthly benefit

Claim at full retirement age and receive your standard amount

Delay until 70 and potentially receive significantly more each month

The right timing depends on your full financial picture, including your health, other retirement income, taxes, lifestyle, and long-term goals.

The Cost of Claiming Too Early

Many people claim Social Security as soon as they are eligible simply because they can. In some cases, that makes sense. But in other situations, claiming early can mean locking in a permanently lower benefit for the rest of your life.

That decision can affect:

Your monthly retirement income

Your spouse’s future survivor benefit

How much you need to withdraw from savings

Your long-term tax picture

This is why Social Security claiming strategies should be part of a broader retirement income plan, not a standalone decision.

Did You Know About Spousal Benefits?

One of the most overlooked parts of Social Security planning is the spousal benefit.

If you are married, you may be eligible to receive up to 50 percent of your spouse’s full retirement benefit, depending on your age and claiming strategy. In some cases, this can create more lifetime income for a household than either spouse expected.

Spousal benefits are often missed because people assume each person simply claims their own benefit and that is the end of the story. That is not always true.

Spousal and survivor benefit rules can play a major role in:

Married couples planning retirement together

One spouse with significantly lower lifetime earnings

Widows and widowers evaluating next steps

Divorced individuals who were married for at least 10 years

Many people are surprised to learn they may have more options than they realized.

Social Security Should Not Be Viewed in Isolation

A strong Social Security strategy should work alongside the rest of your financial life.

That includes:

Investment accounts

401(k), 403(b), and IRA withdrawals

Pension income

Tax planning

Healthcare costs

Estate and legacy goals

For example, taking Social Security earlier may reduce pressure on your investment accounts now, but it could also mean less guaranteed income later. Waiting longer may result in higher monthly income, but only if your other assets can support the delay.

That is why coordination matters.

A North County San Diego Perspective

Retirement planning in North County San Diego comes with its own realities.

From Encinitas and Carlsbad to Del Mar and surrounding communities, many retirees want to remain close to family, enjoy the coastal lifestyle, and maintain flexibility as they age. But higher housing, healthcare, and lifestyle costs can place more pressure on retirement income.

For many local families, Social Security optimization is one of the most practical ways to strengthen a retirement plan without taking on more market risk.

Are You Leaving Money on the Table?

This is the real question.

You may be making a reasonable decision, but is it the best one for your long-term goals? Too often, people make Social Security decisions based on habit, hearsay, or a single rule of thumb.

There is no universal answer. There is only the answer that fits your situation.

Next Steps

Social Security is one of the most important income decisions you will make in retirement. Understanding when to take it, how spousal benefits work, and how it fits into your larger financial plan can make a meaningful difference over time.

If you are approaching retirement or already weighing your options, now is a good time to review your strategy and make sure you are not leaving money on the table.

Independent Wealth Solutions works with individuals, families, and business owners across North County San Diego to build retirement strategies that are thoughtful, personal, and designed for real life.

Contact Independent Wealth Solutions to start a conversation about your retirement income strategy.