Income Impact on Medicare Part B

As you plan ahead for healthcare costs, it is important to understand how your income can directly impact what you pay for Medicare.

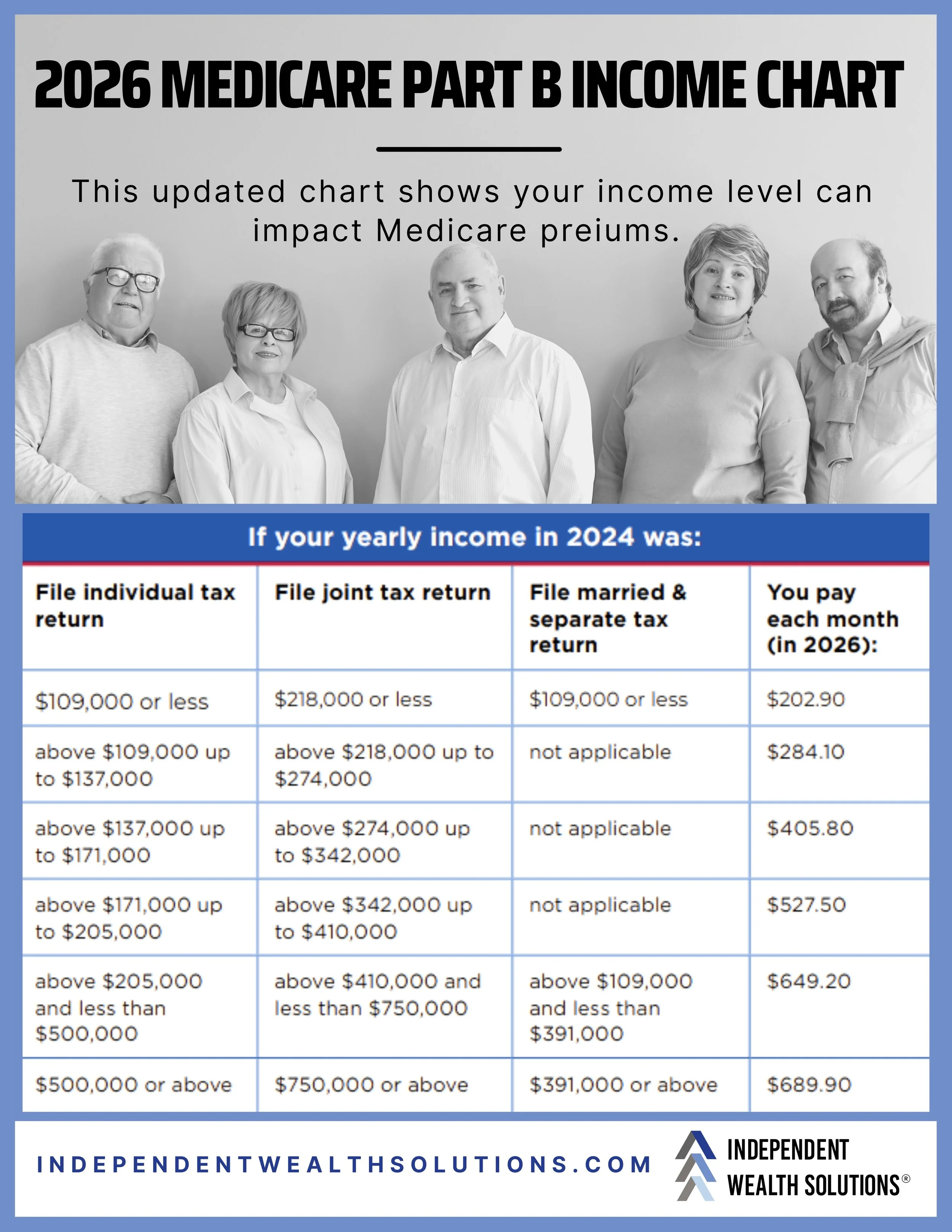

According to the 2026 Medicare Part B income chart, your monthly premium is based on your 2024 tax return (this is because of the Look-Back Rule: Medicare uses a "prior-prior-year" tax rule, meaning 2024 income determines 2026 premiums). If your income exceeds certain thresholds, you may pay an Income-Related Monthly Adjustment Amount, often referred to as IRMAA, in addition to your standard plan premium.

For individuals filing single in 2024, income above $109,000 begins triggering higher monthly premiums in 2026. For married couples filing jointly, the first adjustment begins above $218,000. As income rises through additional tiers, the monthly surcharge increases incrementally. At the highest bracket, individuals earning $500,000 or more, or couples earning $750,000 or more, will see the largest premium adjustments.

What surprises many retirees is that even a one-time spike in income such as a large IRA withdrawal, Roth conversion, capital gain, or property sale can move them into a higher premium bracket two years later.

Proactive income planning can help manage these thresholds. Coordinating distributions, timing Roth conversions carefully, and understanding how Social Security and investment income factor into your Modified Adjusted Gross Income can make a meaningful difference in long-term healthcare costs.

At Independent Wealth Solutions, we work with clients to align retirement income strategies with tax efficiency and Medicare planning. Thoughtful coordination today can help prevent unnecessary premium surprises tomorrow.

If you would like to review how your current income strategy may impact your 2026 Medicare premiums, we are here to help.